I always know when public interest in the crypto market — and broadly in digital assets — is picking up: my phone rings. It’s journalists looking for commentary. Friends looking for tips. Bankers looking for advice.

In 2018, my phone didn’t ring much. In 2019, it rang a bit more often. And now it’s buzzing quite a lot. However, there’s a clear difference between 2017 and now.

This time, there’s no runaway speculative bubble. Instead, we see the steady rise of a market built on firm footings: maturing technology, crystallizing use cases, regulatory tailwinds and growing demand from institutional customers.

This shift that is underway will have a profound impact, especially for financial institutions. Here’s what underpins it and why.

We’re through the digital assets hype cycle

My journey with crypto started in 2011, when I boarded the metaphorical train. I was completing my PhD in mathematical finance with a specialization in high performance computing.

Bitcoin was not so far away from what I was doing, so I started to investigate it and gradually moved into trading it. At the time, there weren’t so many people on the ride with me. It was a risky business: lots of platforms were getting hacked and people, including myself, were regularly losing their coins.

“Bubbles are an essential stage in the development of transformative technologies” — William H. Janeway

But people continued to join in. People like me were intellectually stimulated by the possibilities of trustless, stateless banking as well as the implications of putting law into code through smart contracts.

And so, we worked on developing use cases and applications. At the same time, law enforcers started to weed out some of the worst actors.

The market then started to capture the attention of venture capitalists as well as speculators. And soon, lots of people piled onto the train until it became ridiculously and unsustainably crowded.

The fear of missing out was driving a massive bubble. In Warren Buffet terms, even the shoeshine boy had a crypto portfolio.

When the inevitable crash came, I — like others — stayed on the train and the train has kept moving.

People forget two things about bubbles. First, — as William H. Janeway tells us, bubbles are an essential stage in the development of transformative technologies. They provide funding for the deployment phase. The second thing is that there is always a lag between the installation and deployment periods, which is when people become overexuberant: we overestimate the near-term impact, but underestimate the long term effect.

Metaco Diagram - Digital Assets Hype Cycle

Once the dust of the initial shakeout settles and the hot money is taken away, the time comes to build something stable, strong, with a vision for the long haul.

These conditions are taking crypto into the mainstream

If you got off the train or never joined it at all, here’s an update on what’s been happening.

THE TECHNOLOGY AROUND DIGITAL ASSETS HAS BEEN MATURING

Obviously, security is critical to the integrity of this nascent market. If we can’t keep keys and tokens secure, people won’t feel confident transacting digital assets. But, we now have institutional-grade technology that is:

- built on top of secure hardware and multiparty computation

- scaled to meet the needs of tier 1 banks

- integrated with third-party core banking systems and infrastructure providers

- vetted and implemented by the largest system integrators.

REGULATORY HURDLES ARE DISAPPEARING TOO

Every month, another country passes legislation that clarifies the rules around blockchain and digital assets, easing the passage of these assets into mainstream adoption.

For instance, in July, the US Office of the Comptroller of the Currency (OCC) announced that all federally chartered banks can provide custody service for crypto assets.

Metaco Diagram - Digital Assets Perfect Storm

CENTRAL BANKS ARE ALSO BECOMING INTERESTED IN DIGITAL CURRENCIES,

recognizing the advantages of digital currencies to effectively implement and govern monetary policy. Contrast the situation in the US and China during the pandemic: in the same week that the US government was printing off and posting stimulus checks, the Chinese were beta-testing a digital renminbi in four major cities.

Banks are key to the next phase of digital assets market evolution…

Most importantly, institutional interest in this space is growing strongly. This is where I have a privileged view because we are in discussions with dozens of banks, pretty much everywhere in the world. We see that demand is increasing strongly. Banks and custodians who are investing in digital assets infrastructure will be productive in just a couple of years.

We’ve moved beyond the innovators like Fidelity to the early majority of institutions, like Standard Chartered (a Metaco investor). They recognize that staying competitive and delivering what customers want will require a set of digital assets services underpinned by secure custody.

…and stand to be main beneficiaries

The prize for banks and custodians is massive and comes at a time when many of the existing revenue lines are under attack.

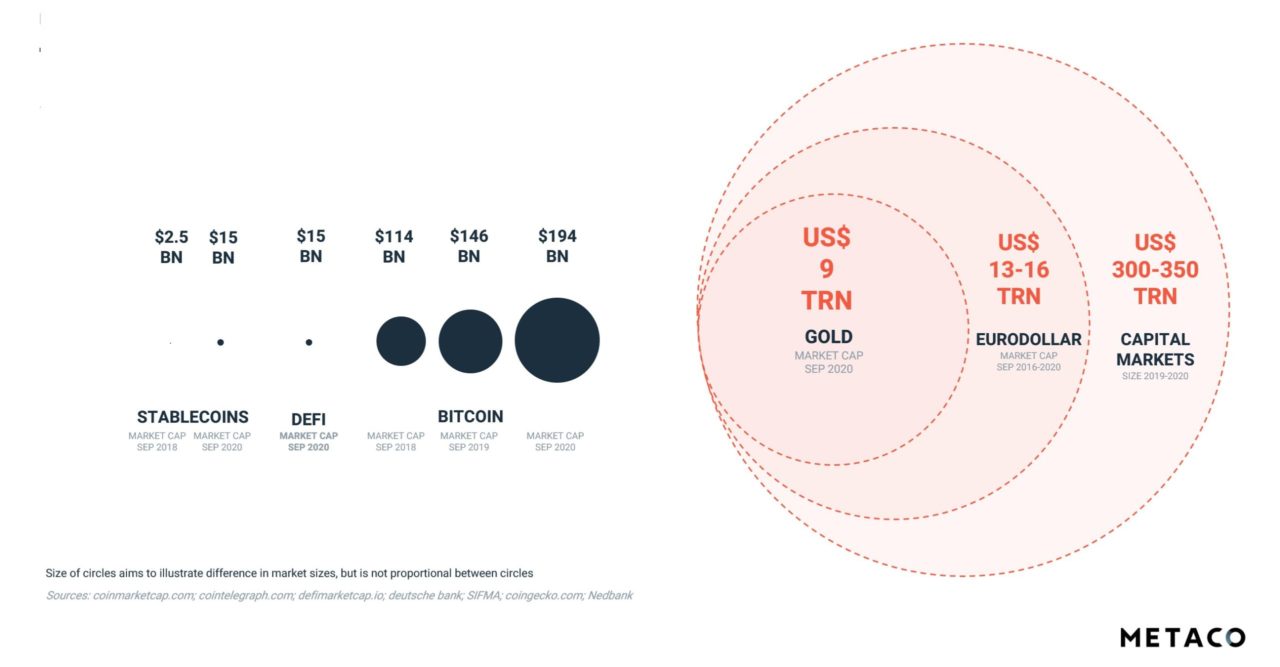

According to the World Economic Forum, the market for tokenized assets alone will hit $24 trillion by 2027, but that’s just the tip of the iceberg. For a comprehensive perspective, look at the market potential more in the context of all capital markets (worth $350 trillion).

Metaco Diagram - Potential Market Size for Digital Assets

Incumbent banks are well positioned to capture this opportunity. They’re trusted (they have been safeguarding client assets for generations), they are already regulated, they’re experts in structured products and capital markets, and they already have large customer bases.

However, moving into digital assets is both an offensive and a defensive move. According to McKinsey, 65% of bank profits today come from distributing and selling banking products (including payments). This is the part of the value chain with the lowest barriers to entry, where banks are losing ground to fintechs and big tech platforms.

So, digital assets represent an opportunity to tap a significant new revenue stream which can more than compensate for revenue lines foregone to new entrants. What’s more, it unlocks access to revenue lines with higher margins and lower asset intensity.

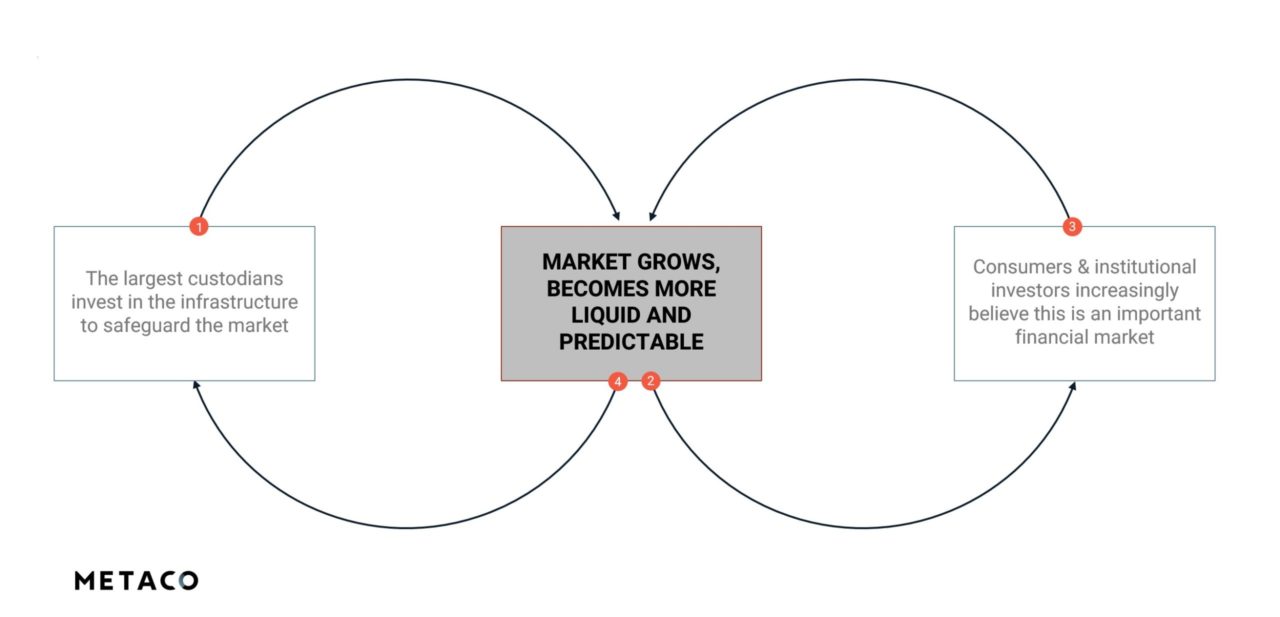

A virtuous cycle is forming

The challenge with the crypto asset market until now has been one of volatility generated by lack of liquidity. Because retail customers and their banks perceived a set of significant risks around these assets, they were reluctant to invest in them (and when they did, it caused a bubble).

Consequently, the investments to underpin the confidence of these retail investors were never made. The large custodians stayed away and it remained a small and volatile market.

However, the situation is now changing. The train kept moving after the crash, the technology matured, the regulatory picture changed.

What’s more, central banks started experimenting and, critically, institutions have been investing in this market ever since.

As a result, we’re moving into a virtuous cycle where, with institutional backing, retail investors and their banks feel increasingly comfortable with investing in this market: already today, over 130m people hold cryptocurrency accounts.

The actions of these players are increasing the liquidity and predictability of digital assets, in turn attracting more institutional and retail investment, thus creating self-reinforcing — and this time sustainable — growth in the digital asset market.

Metaco Diagram - Digital Assets entering a virtuous cycle of exponential growth

Digital assets are finally coming of age!

If you got off the train, there’s still time to get back on. If you never boarded, now is the time. If, until now, no one got fired for ignoring crypto, soon that won’t be the case.